There are more small business financing options than ever before, but the two most popular are still merchant cash advances and term loans. When you apply for these types of products, there are a number of pitfalls you need to avoid in order to ensure you can pay back your financing obligations, achieve your goals, and ultimately grow your business.

However, there is one dangerous practice that impacts the borrower at the time of refinancing (or renewing), rather than borrowing the first time: double dipping. Because it involves carrying over interest from an initial loan (or cash advance) to the next one, it’s a complicated practice to understand for borrowers. How complex is it, exactly? Most borrowers don’t even realize it’s happening.

Typically, a merchant cash advance provider or short term lender will only provide additional capital to a borrower after the current balance is paid in full. Funders will encourage you to refinance and use the money from the next advance or loan to pay off the outstanding balance. If a financing product includes any unpaid interest in the portion of the balance that must be paid off prior to receiving additional capital, or it is not waived when the additional funding interest is added, then it is double dipping.

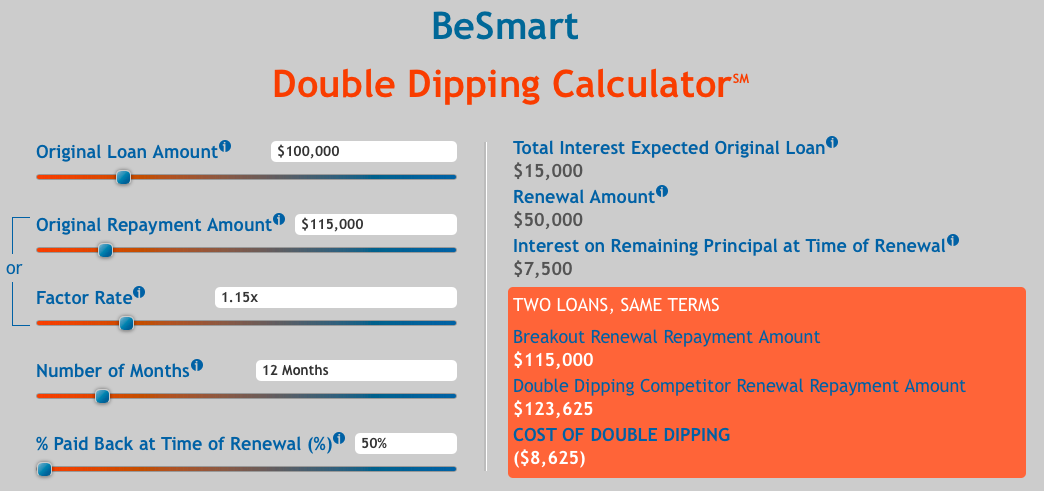

Here is a simplified example, for illustration and educational purposes: a borrower has an original loan amount of $100,000 with a repayment amount of $115,000 over a 12-month period. Halfway through the term of the loan, the borrower elects to renew for an additional $50,000 with the current balance at $57,500 ($50,000 principal/$7,500 remaining interest). The new balance, with the renewal included, should be ($57,500 + $50,000+interest =) $115,000. Instead, a double dipper will include the remaining interest in the final total and then apply new interest to the new total amount ($57,500 + $50,000 = 107,500+interest) of $123,625. In this case, the cost of double dipping to the borrower is $8,625.

This simple example is even more difficult to understand for borrowers if financing providers are unable to communicate the concept in simple terms. If you’re unsure about whether you’re at risk of double dipping, you can use a Double Dipping Calculator with a detailed explainer to help you visualize how this practice works as you facilitate conversations with lenders or cash advance providers.

The financial impact, in terms of interest rate or APR, can be substantial. From a dollars standpoint, double dipping will cost a borrower anywhere from $2,500 to more than $10,000 for each additional renewal or refinancing. But the key is knowing whether you are working with a double dipper before you borrow the first time. Otherwise, you may get stuck in a debt cycle where you are borrowing just to afford to pay what you owe. This should never be the case. Your small business should borrow to grow, and you should achieve the goals you have in place when originally borrowing.

Small business borrower education is paramount, specifically before you agree to any financing. But if you have already borrowed once and are looking to renew an existing loan or advance, start with the following questions:

- Can you explain the proceeds I will receive upon closing the transaction in detail on your payback amount? Ask the lender to provide this in as much detail as possible.

- Can you confirm the unpaid interest (the lender may also refer to this as unpaid fees, factor income, contract amount, or margin income) from the original loan or advance is removed and not added to the new outstanding balance and is not deducted from the proceeds at renewal? If a lender strictly focuses on contract value, you might be working with a double dipper.

- Are you waiving all outstanding interest or fees? Only the outstanding principal should be deducted from the loan proceeds that are sent to you.

Make sure any lender you speak with can provide sufficient answers to these questions and put you at ease. A lender with your best interests in mind will provide free education and evaluate offers for you to help you avoid the pitfalls of double dipping and achieve your business goals.

The post The Impact of Double Dipping on the Small Business Borrower appeared first on Lendio.